Studying

Supervised studying is a class of machine studying that makes use of labeled datasets to coach algorithms to foretell outcomes and acknowledge patterns.

Not like unsupervised studying, supervised studying algorithms are given labeled coaching to be taught the connection between the enter and the outputs.

Prerequisite: Linear algebra

Suppose we’ve a regression downside the place the mannequin must predict steady values by taking n variety of enter options (xi).

The prediction worth is outlined as a operate referred to as speculation (h):

the place:

- θi: i-th parameter corresponding to every enter function (x_i),

- ϵ (epsilon): Gaussian error (ϵ ~ N(0, σ²)))

Because the speculation for a single enter generates a scalar worth (hθ(x)∈R), it may be denoted because the dot product of the transpose of the parameter vector (θT) and the function vector for that enter (x):

Batch Gradient Descent

Gradient Descent is an iterative optimization algorithm used to seek out native minima of a operate. At every step, it strikes within the course reverse to the course of steepest descent to progressively decrease the operate’s worth — merely, maintain going downhill.

Now, recall we’ve n parameters that impression the prediction. So, we have to know the precise contribution of the particular person parameter (θi) akin to coaching information (xi)) to the operate.

Suppose we set measurement of every step as a studying charge (α), and discover a value curve (J), then the parameter is deducted at every step such that:

(α: studying charge, J(θ): cost operate, ∂/∂θi: partial by-product of the associated fee operate with respect to θi)

Gradient

The gradient represents the slope of the associated fee operate.

Contemplating the remaining parameters and their corresponding partial derivatives of the associated fee operate (J), the gradient of the associated fee operate at θ for n parameters is outlined as:

Gradient is a matrix notation of partial derivatives of the associated fee operate with respect to all of the parameters (θ0 to θn).

Because the studying charge is a scalar (α∈R), the replace rule of the gradient descent algorithm is expressed in matrix notation:

Consequently, the parameter (θ) resides within the (n+1)-dimensional area.

Geographically, it goes downhill at a step akin to the training charge till reaching the convergence.

Computation

The target of linear regression is to attenuate the hole (MSE) between predicted values and precise values given within the coaching dataset.

Price Perform (Goal Perform)

This hole (MSE) is outlined as a median hole of all of the coaching examples:

the place

- Jθ: value operate (or loss operate),

- hθ: prediction from the mannequin,

- x: i_th enter function,

- y: i_th goal worth, and

- m: the variety of coaching examples.

The gradient is computed by taking partial by-product of the associated fee operate with respect to every parameter:

As a result of we’ve n+1 parameters (together with an intercept time period θ0) and m coaching examples, we’ll kind a gradient vector utilizing matrix notation:

In matrix notation, the place X represents the design matrix together with the intercept time period and θ is the parameter vector, the gradient ∇θJ(θ) is given by:

The LMS (Least Imply Squares) rule is an iterative algorithm that repeatedly adjusts the mannequin’s parameters primarily based on the error between its predictions and the precise goal values of the coaching examples.

Least Minimal Squares (LMS) Rule

In every epoch of gradient descent, each parameter θi is up to date by subtracting a fraction of the typical error throughout all coaching examples:

This course of permits the algorithm to iteratively discover the optimum parameters that decrease the associated fee operate.

(Be aware: θi is a parameter related to enter function xi, and the aim of the algorithm is to seek out its optimum worth, not that it’s already an optimum parameter.)

Regular Equation

To search out the optimum parameter (θ*) that minimizes the associated fee operate, we will use the regular equation.

This technique gives an analytical answer for linear regression, permitting us to instantly calculate the θ worth that minimizes the associated fee operate.

Not like iterative optimization strategies, the traditional equation finds this optimum by instantly fixing for the purpose the place the gradient is zero, guaranteeing quick convergence:

Therefore:

This depends on the belief that the design matrix X is invertible, which means that every one its enter options (from x_0 to x_n) are linearly impartial.

If X is just not invertible, we’ll want to regulate the enter options to make sure their mutual independence.

Simulation

In actuality, we repeat the method till convergence by setting:

- Price operate and its gradient

- Studying charge

- Tolerance (min. value threshold to cease the iteration)

- Most variety of iterations

- Place to begin

Batch by Studying Charge

The next coding snippet demonstrates the method of gradient descent finds native minima of a quadratic value operate by studying charges (0.1, 0.3, 0.8 and 0.9):

def cost_func(x):

return x**2 - 4 * x + 1

def gradient(x):

return 2*x - 4

def gradient_descent(gradient, begin, learn_rate, max_iter, tol):

x = begin

steps = [start] # information studying steps

for _ in vary(max_iter):

diff = learn_rate * gradient(x)

if np.abs(diff) < tol:

break

x = x - diff

steps.append(x)

return x, steps

x_values = np.linspace(-4, 11, 400)

y_values = cost_func(x_values)

initial_x = 9

iterations = 100

tolerance = 1e-6

learning_rates = [0.1, 0.3, 0.8, 0.9]

def gradient_descent_curve(ax, learning_rate):

final_x, historical past = gradient_descent(gradient, initial_x, learning_rate, iterations, tolerance)

ax.plot(x_values, y_values, label=f'Price operate: $J(x) = x^2 - 4x + 1$', lw=1, shade='black')

ax.scatter(historical past, [cost_func(x) for x in history], shade='pink', zorder=5, label='Steps')

ax.plot(historical past, [cost_func(x) for x in history], 'r--', lw=1, zorder=5)

ax.annotate('Begin', xy=(historical past[0], cost_func(historical past[0])), xytext=(historical past[0], cost_func(historical past[0]) + 10),

arrowprops=dict(facecolor='black', shrink=0.05), ha='heart')

ax.annotate('Finish', xy=(final_x, cost_func(final_x)), xytext=(final_x, cost_func(final_x) + 10),

arrowprops=dict(facecolor='black', shrink=0.05), ha='heart')

ax.set_title(f'Studying Charge: {learning_rate}')

ax.set_xlabel('Enter function: x')

ax.set_ylabel('Price: J')

ax.grid(True, alpha=0.5, ls='--', shade='gray')

ax.legend()

fig, axs = plt.subplots(1, 4, figsize=(30, 5))

fig.suptitle('Gradient Descent Steps by Studying Charge')

for ax, lr in zip(axs.flatten(), learning_rates):

gradient_descent_curve(ax=ax, learning_rate=lr)

Predicting Credit score Card Transaction

Allow us to use a sample dataset on Kaggle to foretell bank card transaction utilizing linear regression with Batch GD.

1. Knowledge Preprocessing

a) Base DataFrame

First, we’ll merge these 4 information from the pattern dataset utilizing IDs as the important thing, whereas sanitizing the uncooked information:

- transaction (csv)

- person (csv)

- bank card (csv)

- train_fraud_labels (json)

# load transaction information

trx_df = pd.read_csv(f'{dir}/transactions_data.csv')

# sanitize the dataset

trx_df = trx_df[trx_df['errors'].isna()]

trx_df = trx_df.drop(columns=['merchant_city','merchant_state', 'date', 'mcc', 'errors'], axis='columns')

trx_df['amount'] = trx_df['amount'].apply(sanitize_df)

# merge the dataframe with fraud transaction flag.

with open(f'{dir}/train_fraud_labels.json', 'r') as fp:

fraud_labels_json = json.load(fp=fp)

fraud_labels_dict = fraud_labels_json.get('goal', {})

fraud_labels_series = pd.Collection(fraud_labels_dict, title='is_fraud')

fraud_labels_series.index = fraud_labels_series.index.astype(int)

merged_df = pd.merge(trx_df, fraud_labels_series, left_on='id', right_index=True, how='left')

merged_df.fillna({'is_fraud': 'No'}, inplace=True)

merged_df['is_fraud'] = merged_df['is_fraud'].map({'Sure': 1, 'No': 0})

merged_df = merged_df.dropna()

# load card information

card_df = pd.read_csv(f'{dir}/cards_data.csv')

card_df = card_df.substitute('nan', np.nan).dropna()

card_df = card_df[card_df['card_on_dark_web'] == 'No']

card_df = card_df.drop(columns=['acct_open_date', 'card_number', 'expires', 'cvv', 'card_on_dark_web'], axis='columns')

card_df['credit_limit'] = card_df['credit_limit'].apply(sanitize_df)

# load person information

user_df = pd.read_csv(f'{dir}/users_data.csv')

user_df = user_df.drop(columns=['birth_year', 'birth_month', 'address', 'latitude', 'longitude'], axis='columns')

user_df = user_df.substitute('nan', np.nan).dropna()

user_df['per_capita_income'] = user_df['per_capita_income'].apply(sanitize_df)

user_df['yearly_income'] = user_df['yearly_income'].apply(sanitize_df)

user_df['total_debt'] = user_df['total_debt'].apply(sanitize_df)

# merge transaction and card information

merged_df = pd.merge(left=merged_df, proper=card_df, left_on='card_id', right_on='id', how='interior')

merged_df = pd.merge(left=merged_df, proper=user_df, left_on='client_id_x', right_on='id', how='interior')

merged_df = merged_df.drop(columns=['id_x', 'client_id_x', 'card_id', 'merchant_id', 'id_y', 'client_id_y', 'id'], axis='columns')

merged_df = merged_df.dropna()

# finalize the dataframe

categorical_cols = merged_df.select_dtypes(embody=['object']).columns

df = merged_df.copy()

df = pd.get_dummies(df, columns=categorical_cols, dummy_na=False, dtype=float)

df = df.dropna()

print('Base information body: n', df.head(n=3))

b) Preprocessing

From the bottom DataFrame, we’ll select appropriate enter options with:

steady values, and seemingly linear relationship with transaction quantity.

df = df[df['is_fraud'] == 0]

df = df[['amount', 'per_capita_income', 'yearly_income', 'credit_limit', 'credit_score', 'current_age']]Then, we’ll filter outliers past 3 customary deviations away from the imply:

def filter_outliers(df, column, std_threshold) -> pd.DataFrame:

imply = df[column].imply()

std = df[column].std()

upper_bound = imply + std_threshold * std

lower_bound = imply - std_threshold * std

filtered_df = df[(df[column] <= upper_bound) | (df[column] >= lower_bound)]

return filtered_df

df = df.substitute(to_replace='NaN', worth=0)

df = filter_outliers(df=df, column='quantity', std_threshold=3)

df = filter_outliers(df=df, column='per_capita_income', std_threshold=3)

df = filter_outliers(df=df, column='credit_limit', std_threshold=3)Lastly, we’ll take the logarithm of the goal worth quantity to mitigate skewed distribution:

df['amount'] = df['amount'] + 1

df['amount_log'] = np.log(df['amount'])

df = df.drop(columns=['amount'], axis='columns')

df = df.dropna()*Added one to quantity to keep away from unfavourable infinity in amount_log column.

Closing DataFrame:

c) Transformer

Now, we will cut up and rework the ultimate DataFrame into practice/check datasets:

categorical_features = X.select_dtypes(embody=['object']).columns.tolist()

categorical_transformer = Pipeline(steps=[('imputer', SimpleImputer(strategy='most_frequent')),('onehot', OneHotEncoder(handle_unknown='ignore'))])

numerical_features = X.select_dtypes(embody=['int64', 'float64']).columns.tolist()

numerical_transformer = Pipeline(steps=[('imputer', SimpleImputer(strategy='mean')), ('scaler', StandardScaler())])

preprocessor = ColumnTransformer(

transformers=[

('num', numerical_transformer, numerical_features),

('cat', categorical_transformer, categorical_features)

]

)

X_train_processed = preprocessor.fit_transform(X_train)

X_test_processed = preprocessor.rework(X_test)2. Defining Batch GD Regresser

class BatchGradientDescentLinearRegressor:

def __init__(self, learning_rate=0.01, n_iterations=1000, l2_penalty=0.01, tol=1e-4, persistence=10):

self.learning_rate = learning_rate

self.n_iterations = n_iterations

self.l2_penalty = l2_penalty

self.tol = tol

self.persistence = persistence

self.weights = None

self.bias = None

self.historical past = {'loss': [], 'grad_norm': [], 'weight':[], 'bias': [], 'val_loss': []}

self.best_weights = None

self.best_bias = None

self.best_val_loss = float('inf')

self.epochs_no_improve = 0

def _mse_loss(self, y_true, y_pred, weights):

m = len(y_true)

loss = (1 / (2 * m)) * np.sum((y_pred - y_true)**2)

l2_term = (self.l2_penalty / (2 * m)) * np.sum(weights**2)

return loss + l2_term

def match(self, X_train, y_train, X_val=None, y_val=None):

n_samples, n_features = X_train.form

self.weights = np.zeros(n_features)

self.bias = 0

for i in vary(self.n_iterations):

y_pred = np.dot(X_train, self.weights) + self.bias

dw = (1 / n_samples) * np.dot(X_train.T, (y_pred - y_train)) + (self.l2_penalty / n_samples) * self.weights

db = (1 / n_samples) * np.sum(y_pred - y_train)

loss = self._mse_loss(y_train, y_pred, self.weights)

gradient = np.concatenate([dw, [db]])

grad_norm = np.linalg.norm(gradient)

# replace historical past

self.historical past['weight'].append(self.weights[0])

self.historical past['loss'].append(loss)

self.historical past['grad_norm'].append(grad_norm)

self.historical past['bias'].append(self.bias)

# descent

self.weights -= self.learning_rate * dw

self.bias -= self.learning_rate * db

if X_val is just not None and y_val is just not None:

val_y_pred = np.dot(X_val, self.weights) + self.bias

val_loss = self._mse_loss(y_val, val_y_pred, self.weights)

self.historical past['val_loss'].append(val_loss)

if val_loss < self.best_val_loss - self.tol:

self.best_val_loss = val_loss

self.best_weights = self.weights.copy()

self.best_bias = self.bias

self.epochs_no_improve = 0

else:

self.epochs_no_improve += 1

if self.epochs_no_improve >= self.persistence:

print(f"Early stopping at iteration {i+1} (validation loss didn't enhance for {self.persistence} epochs)")

self.weights = self.best_weights

self.bias = self.best_bias

break

if (i + 1) % 100 == 0:

print(f"Iteration {i+1}/{self.n_iterations}, Loss: {loss:.4f}", finish="")

if X_val is just not None:

print(f", Validation Loss: {val_loss:.4f}")

else:

go

def predict(self, X_test):

return np.dot(X_test, self.weights) + self.bias3. Prediction & Evaluation

mannequin = BatchGradientDescentLinearRegressor(learning_rate=0.001, n_iterations=10000, l2_penalty=0, tol=1e-5, persistence=5)

mannequin.match(X_train_processed, y_train.values)

y_pred = mannequin.predict(X_test_processed)Output:

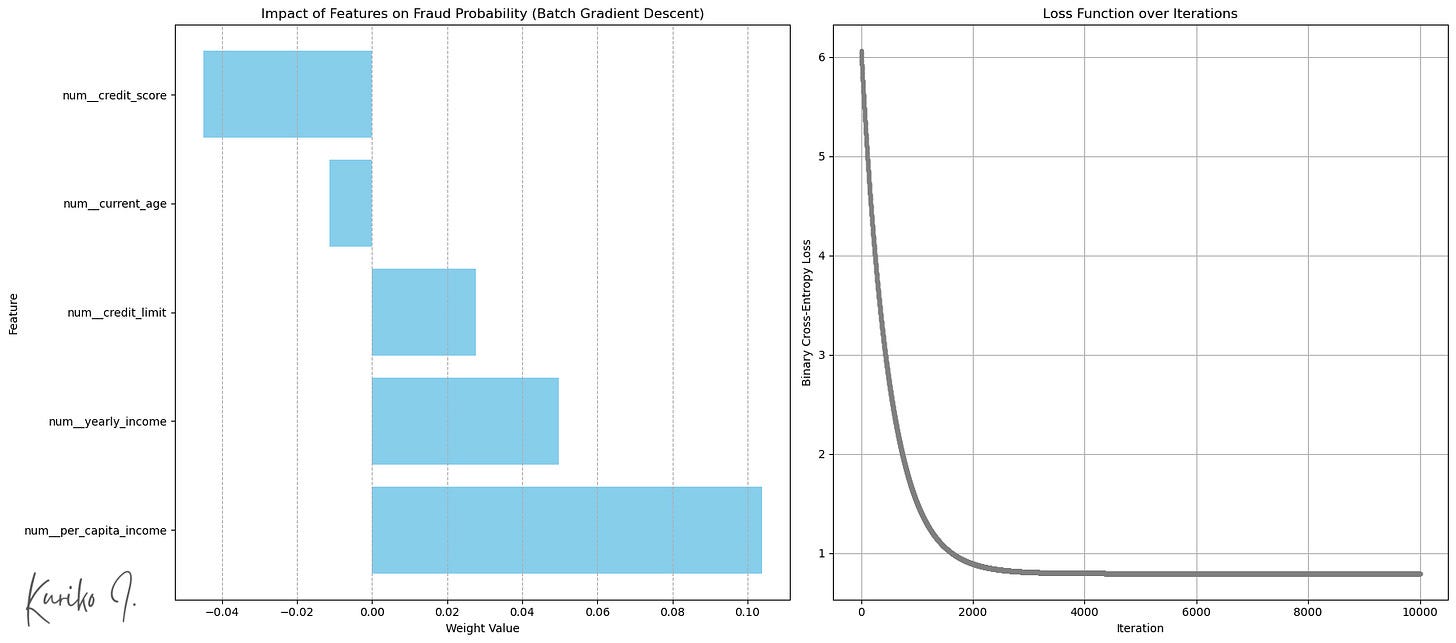

Of the 5 enter options, per_capita_income confirmed the very best correlation with the transaction quantity:

(Left: Weight by enter options (Backside: extra transaction), Proper: Price operate (learning_rate=0.001, i=10,000, m=50,000, n=5))

Imply Squared Error (MSE): 1.5752

R-squared: 0.0206

Imply Absolute Error (MAE): 1.0472

Time complexity: Coaching: O(n²m+n³) + Prediction: O(n)

House complexity: O(nm)

(m: coaching instance measurement, n: enter function measurement, assuming m >>> n)

Stochastic Gradient Descent

Batch GD makes use of all the coaching dataset to compute gradient in every iteration step (epoch), which is computationally costly particularly when we’ve hundreds of thousands of dataset.

Stochastic Gradient Descent (SGD) alternatively,

- sometimes shuffles the coaching information initially of every epoch,

- randomly choose a single coaching instance in every iteration,

- calculates the gradient utilizing the instance, and

- updates the mannequin’s weights and bias after processing every particular person coaching instance.

This leads to many weight updates per epoch (equal to the variety of coaching samples), many fast and computationally low cost updates primarily based on particular person information factors, permitting it to iterate by means of giant datasets a lot quicker.

Simulation

Much like Batch GD, we’ll outline the SGD class and run the prediction:

class StochasticGradientDescentLinearRegressor:

def __init__(self, learning_rate=0.01, n_iterations=100, l2_penalty=0.01, random_state=None):

self.learning_rate = learning_rate

self.n_iterations = n_iterations

self.l2_penalty = l2_penalty

self.random_state = random_state

self._rng = np.random.default_rng(seed=random_state)

self.weights_history = []

self.bias_history = []

self.loss_history = []

self.weights = None

self.bias = None

def _mse_loss_single(self, y_true, y_pred):

return 0.5 * (y_pred - y_true)**2

def match(self, X, y):

n_samples, n_features = X.form

self.weights = self._rng.random(n_features)

self.bias = 0.0

for epoch in vary(self.n_iterations):

permutation = self._rng.permutation(n_samples)

X_shuffled = X[permutation]

y_shuffled = y[permutation]

epoch_loss = 0

for i in vary(n_samples):

xi = X_shuffled[i]

yi = y_shuffled[i]

y_pred = np.dot(xi, self.weights) + self.bias

dw = xi * (y_pred - yi) + self.l2_penalty * self.weights

db = y_pred - yi

self.weights -= self.learning_rate * dw

self.bias -= self.learning_rate * db

epoch_loss += self._mse_loss_single(yi, y_pred)

if n_features >= 2:

self.weights_history.append(self.weights[:2].copy())

elif n_features == 1:

self.weights_history.append(np.array([self.weights[0], 0]))

self.bias_history.append(self.bias)

self.loss_history.append(self._mse_loss_single(yi, y_pred) + (self.l2_penalty / (2 * n_samples)) * (np.sum(self.weights**2) + self.bias**2)) # Approx L2

print(f"Epoch {epoch+1}/{self.n_iterations}, Loss: {epoch_loss/n_samples:.4f}")

def predict(self, X):

return np.dot(X, self.weights) + self.bias

mannequin = StochasticGradientDescentLinearRegressor(learning_rate=0.001, n_iterations=200, random_state=42)

mannequin.match(X=X_train_processed, y=y_train.values)

y_pred = mannequin.predict(X_test_processed)Output:

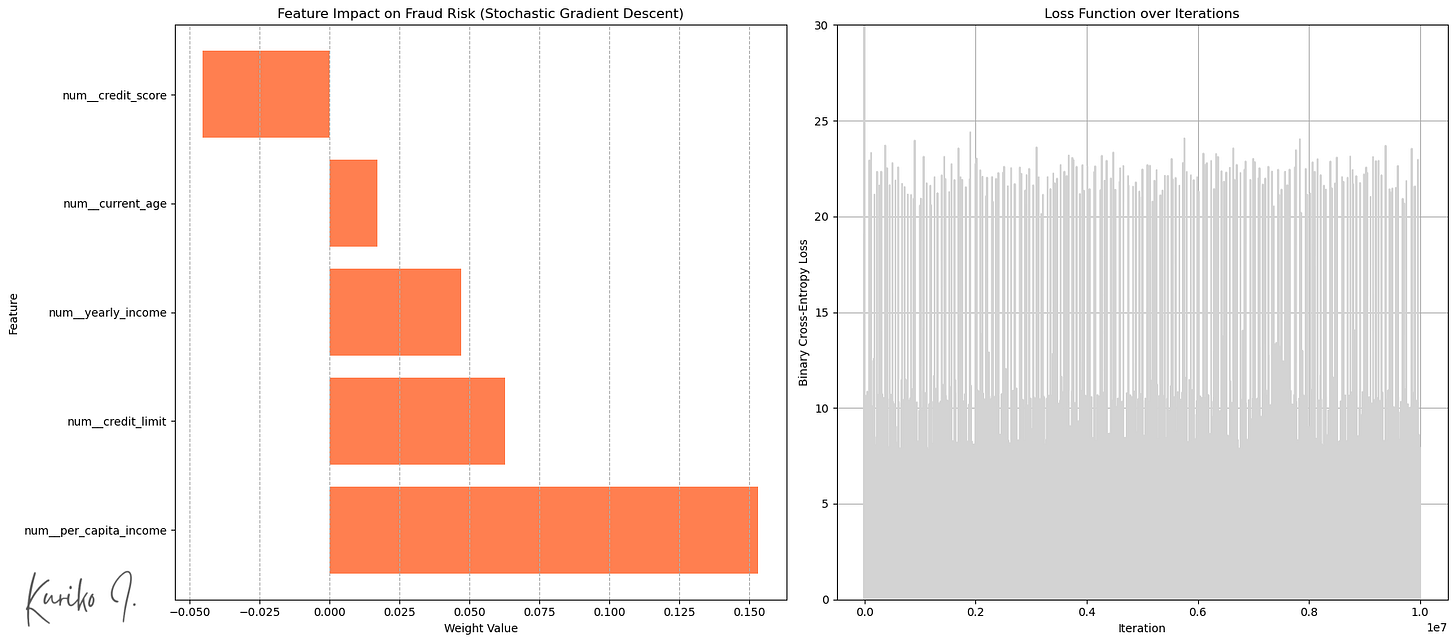

Left: Weight by enter options, Proper: Price operate (learning_rate=0.001, i=200, m=50,000, n=5)

SGD launched randomness into the optimization course of (fig. proper).

This “noise” will help the algorithm bounce out of shallow native minima or saddle factors and doubtlessly discover higher areas of the parameter area.

Outcomes:

Imply Squared Error (MSE): 1.5808

R-squared: 0.0172

Imply Absolute Error (MAE): 1.0475

Time complexity: Coaching: O(n²m+n³) + Prediction: O(n)

House complexity: O(n) < BGD: O(nm)

(m: coaching instance measurement, n: enter function measurement, assuming m >>> n)

Conclusion

Whereas the easy linear mannequin is computationally environment friendly, its inherent simplicity typically prevents it from capturing complicated relationships throughout the information.

Contemplating the trade-offs of assorted modeling approaches towards particular targets is crucial for attaining optimum outcomes.

Reference

All photographs, except in any other case famous, are by the writer.

The article makes use of artificial information, licensed under Apache 2.0 for commercial use.

Creator: Kuriko IWAI